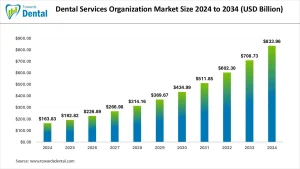

The global dental services organization market was valued at USD 163.83 billion in 2024 and is expected to reach USD 833.96 billion by 2034, growing at a CAGR of 17.67%, driven by rising demand for organized dental care and advanced oral health solutions.

Dental Services Organization Market Statical Scope

By Service

- Human Resources

- Medical Supplies Procurement

- Marketing

- Accounting

- Legal Services

By End User

- General Dentists

- Dental Surgeons

- Orthodontists

- Endodontists

- Oral Surgeons

By Practice Size

- Solo Practices

- Small Groups

- Large Groups

- Multi-location Networks

By Ownership Model

- Private Equity

- Corporate

- Partnership

- Independent DSOs

List of Table and Figure

List of Tables

- Table 1: Global Dental Services Organization Market Size (USD Billion) by Service, 2024–2034

- Table 2: Global Dental Services Organization Market Size (USD Billion) by End User, 2024–2034

- Table 3: Global Dental Services Organization Market Size (USD Billion) by Practice Size, 2024–2034

- Table 4: Global Dental Services Organization Market Size (USD Billion) by Ownership Model, 2024–2034

- Table 5: North America Dental Services Organization Market Size (USD Billion) by Service, 2024–2034

- Table 6: North America Dental Services Organization Market Size (USD Billion) by End User, 2024–2034

- Table 7: North America Dental Services Organization Market Size (USD Billion) by Practice Size, 2024–2034

- Table 8: North America Dental Services Organization Market Size (USD Billion) by Ownership Model, 2024–2034

- Table 9: U.S. Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 10: Canada Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 11: Mexico Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 12: Europe Dental Services Organization Market Size (USD Billion) by Service, 2024–2034

- Table 13: Europe Dental Services Organization Market Size (USD Billion) by End User, 2024–2034

- Table 14: Germany Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 15: France Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 16: UK Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 17: Italy Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 18: Asia Pacific Dental Services Organization Market Size (USD Billion) by Service, 2024–2034

- Table 19: Asia Pacific Dental Services Organization Market Size (USD Billion) by End User, 2024–2034

- Table 20: China Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 21: Japan Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 22: India Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 23: South Korea Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 24: Southeast Asia Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 25: Latin America Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 26: Brazil Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 27: Middle East & Africa Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 28: GCC Countries Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 29: Turkey Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

- Table 30: Africa Dental Services Organization Market Size (USD Billion) by Service & End User, 2024–2034

List of Figures

- Figure 1: Global Dental Services Organization Market Share by Service, 2024

- Figure 2: Global Dental Services Organization Market Share by End User, 2024

- Figure 3: Global Dental Services Organization Market Share by Practice Size, 2024

- Figure 4: Global Dental Services Organization Market Share by Ownership Model, 2024

- Figure 5: North America Dental Services Organization Market Share by Service, 2024

- Figure 6: North America Dental Services Organization Market Share by End User, 2024

- Figure 7: North America Dental Services Organization Market Share by Practice Size, 2024

- Figure 8: North America Dental Services Organization Market Share by Ownership Model, 2024

- Figure 9: U.S. Dental Services Organization Market Share by Service, 2024

- Figure 10: U.S. Dental Services Organization Market Share by End User, 2024

- Figure 11: Canada Dental Services Organization Market Share by Service, 2024

- Figure 12: Canada Dental Services Organization Market Share by End User, 2024

- Figure 13: Mexico Dental Services Organization Market Share by Service, 2024

- Figure 14: Mexico Dental Services Organization Market Share by End User, 2024

- Figure 15: Europe Dental Services Organization Market Share by Service, 2024

- Figure 16: Europe Dental Services Organization Market Share by End User, 2024

- Figure 17: Germany Dental Services Organization Market Share by Service, 2024

- Figure 18: Germany Dental Services Organization Market Share by End User, 2024

- Figure 19: France Dental Services Organization Market Share by Service, 2024

- Figure 20: France Dental Services Organization Market Share by End User, 2024

- Figure 21: UK Dental Services Organization Market Share by Service, 2024

- Figure 22: UK Dental Services Organization Market Share by End User, 2024

- Figure 23: Italy Dental Services Organization Market Share by Service, 2024

- Figure 24: Italy Dental Services Organization Market Share by End User, 2024

- Figure 25: Asia Pacific Dental Services Organization Market Share by Service, 2024

- Figure 26: Asia Pacific Dental Services Organization Market Share by End User, 2024

- Figure 27: China Dental Services Organization Market Share by Service, 2024

- Figure 28: China Dental Services Organization Market Share by End User, 2024

- Figure 29: Japan Dental Services Organization Market Share by Service, 2024

- Figure 30: Japan Dental Services Organization Market Share by End User, 2024

- Figure 31: India Dental Services Organization Market Share by Service, 2024

- Figure 32: India Dental Services Organization Market Share by End User, 2024

- Figure 33: South Korea Dental Services Organization Market Share by Service, 2024

- Figure 34: South Korea Dental Services Organization Market Share by End User, 2024

- Figure 35: Southeast Asia Dental Services Organization Market Share by Service, 2024

- Figure 36: Southeast Asia Dental Services Organization Market Share by End User, 2024

- Figure 37: Latin America Dental Services Organization Market Share by Service, 2024

- Figure 38: Latin America Dental Services Organization Market Share by End User, 2024

- Figure 39: Brazil Dental Services Organization Market Share by Service, 2024

- Figure 40: Brazil Dental Services Organization Market Share by End User, 2024

- Figure 41: Middle East & Africa Dental Services Organization Market Share by Service, 2024

- Figure 42: Middle East & Africa Dental Services Organization Market Share by End User, 2024

- Figure 43: GCC Countries Dental Services Organization Market Share by Service, 2024

- Figure 44: GCC Countries Dental Services Organization Market Share by End User, 2024

- Figure 45: Turkey Dental Services Organization Market Share by Service, 2024

- Figure 46: Turkey Dental Services Organization Market Share by End User, 2024

- Figure 47: Africa Dental Services Organization Market Share by Service, 2024

- Figure 48: Africa Dental Services Organization Market Share by End User, 2024

Principal Research Analyst | Towards Dental

Rohan Patil stands at the forefront of dental market research, leveraging over five years of specialized experience to navigate the intricate landscape of the global dental industry. As Principal Research Analyst at Towards Dental, he spearheads comprehensive research initiatives that encompass a broad spectrum of dental sectors, including orthodontics, periodontics, prosthodontics, and endodontics.

At Towards Dental, Rohan's expertise extends to analyzing emerging trends in dental technologies, regulatory frameworks, and market dynamics. He is instrumental in assessing the adoption of digital dentistry, advancements in dental materials, and the integration of artificial intelligence in diagnostic and treatment modalities.

Rohan's analytical acumen is complemented by his proficiency in translating complex data into actionable insights, enabling him to provide strategic recommendations that inform decision-making across the dental industry. His work not only supports dental professionals and organizations but also contributes to shaping the future trajectory of dental care globally. A trusted advisor and relentless innovator, Rohan continues to push the boundaries of traditional market research, merging scientific rigor with commercial insight to stay ahead in a fast-evolving dental landscape.

Rohan Patil stands at the forefront of dental market research, leveraging over five years of specialized experience to navigate the intricate landscape of the global dental industry. As Principal Research Analyst at Towards Dental, he spearheads comprehensive research initiatives that encompass a broad spectrum of dental sectors, including orthodontics, periodontics, prosthodontics, and endodontics.

At Towards Dental, Rohan's expertise extends to analyzing emerging trends in dental technologies, regulatory frameworks, and market dynamics. He is instrumental in assessing the adoption of digital dentistry, advancements in dental materials, and the integration of artificial intelligence in diagnostic and treatment modalities.

Rohan's analytical acumen is complemented by his proficiency in translating complex data into actionable insights, enabling him to provide strategic recommendations that inform decision-making across the dental industry. His work not only supports dental professionals and organizations but also contributes to shaping the future trajectory of dental care globally. A trusted advisor and relentless innovator, Rohan continues to push the boundaries of traditional market research, merging scientific rigor with commercial insight to stay ahead in a fast-evolving dental landscape.

Latest posts by Rohan Patil (see all)

- Mobile Dental Unit Market Size to Attain USD 3.76 Billion by 2034 - January 6, 2026

- Dental Cone Beam CT Market Size to Attain USD 1,247.49 Million by 2034 - January 5, 2026

- Dental Resins Market Size to Lead USD 2.7 Billion by 2034 - January 2, 2026