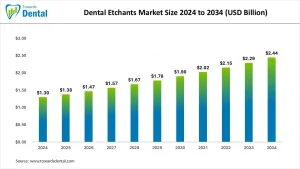

The dental etchants market was valued at USD 1.3 billion in 2024 and is projected to reach nearly USD 2.44 billion by 2034, expanding at a 6.5% CAGR. Growth is fueled by rising restorative procedures and advances in adhesive dentistry.

What Key Market Drivers, Opportunities, and Challenges Are Shaping the Growth of Dental Etchants?

The dental etchants market includes phosphoric acid gels, liquid conditioners, and general-purpose etching systems to prepare enamel and dentin surfaces for bonding restorative materials, sealants, cements, and glues. Etchants increase the retention of micromechanical bonds, bond strength, and the long-term stability of fillings, veneers, crowns, bridges, orthodontic brackets, and minimal-invasive aesthetic operations.

The opportunity environment is broadened through minimal-invasive patient cavity preparations, the expansion of pediatric sealing processes, and the extensive application of adhesive protocols in trauma care, periodontal reconstruction, and pre-implant restorative planning. In less affluent areas, fewer adhesive dentistry products are adopted, fewer restorations are based on amalgam, and fewer high-quality etching systems are used, thus reducing market penetration. The care of the environment through the disposal of chemicals and the lack of trained clinicians in superior bonding methods are additional issues that complicate widespread adoption, but the current innovation continues to support the future development of the market.

How Do Regional Trends Influence the Adoption of Dental Etchants Worldwide?

North America controls the dental etchants market due to high adherence to adhesive dentistry, a high volume of restorative and cosmetic procedures, and a high rate of composite-based restorations over traditional restorations. The United States has the largest number of specialty practices, sophisticated dental education programs, and stable demand for high-performance etching departments in restorative, orthodontic, and prosthodontic processes.

Europe is close behind, with high consumption in Germany, France, Italy, the UK, and the Nordic region, and solid dental manufacturing capacity, comprehensive regulatory oversight, and early adoption of minimally invasive adhesive protocols. The Asia-Pacific region is the most rapidly developing market, with soaring disposable incomes, dental tourism proliferating, and composite restorations replacing older material options in India, China, Thailand, South Korea, and Japan.

How Are AI, Digital Workflows, and Advanced Diagnostic Technologies Transforming the Dental Etchants Market?

The dental etchants market is changing with the introduction of AI and digital technologies to improve formulation science, precision dispensing mechanisms, and procedural precision. The AI-based training systems mimic etching depth, surface conditioning, and bonding procedures and enhance clinicians’ clinical competence in addressing variations in enamel and dentin substrates.

Digital workflow integration enables etchants to be synchronized with CAD/CAM restorative systems, ensuring uniform bonding of digitally designed restorations and veneers. The AI-supported diagnostic tools that can evaluate enamel integrity, detect the need to selectively etch areas, and advise clinicians on the least invasive restoration

method are especially useful, especially when used in conjunction with CBCT and intraoral scanners.

Dental Etchants Market Statical Scope

By Product Type

- Total Etch

- Self-Etch

- Selective Etch

Rohan Patil stands at the forefront of dental market research, leveraging over five years of specialized experience to navigate the intricate landscape of the global dental industry. As Principal Research Analyst at Towards Dental, he spearheads comprehensive research initiatives that encompass a broad spectrum of dental sectors, including orthodontics, periodontics, prosthodontics, and endodontics.

At Towards Dental, Rohan's expertise extends to analyzing emerging trends in dental technologies, regulatory frameworks, and market dynamics. He is instrumental in assessing the adoption of digital dentistry, advancements in dental materials, and the integration of artificial intelligence in diagnostic and treatment modalities.

Rohan's analytical acumen is complemented by his proficiency in translating complex data into actionable insights, enabling him to provide strategic recommendations that inform decision-making across the dental industry. His work not only supports dental professionals and organizations but also contributes to shaping the future trajectory of dental care globally. A trusted advisor and relentless innovator, Rohan continues to push the boundaries of traditional market research, merging scientific rigor with commercial insight to stay ahead in a fast-evolving dental landscape.

- Mobile Dental Unit Market Size to Attain USD 3.76 Billion by 2034 - January 6, 2026

- Dental Cone Beam CT Market Size to Attain USD 1,247.49 Million by 2034 - January 5, 2026

- Dental Resins Market Size to Lead USD 2.7 Billion by 2034 - January 2, 2026