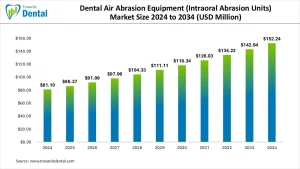

The dental air abrasion equipment market was valued at USD 81.1 million in 2024 and is expected to reach USD 152.24 million by 2034 at a CAGR of 6.5%, driven by minimally invasive dentistry trends and rising adoption of intraoral abrasion units.

Why Is There High Demand in the Dental Air Abrasion Equipment Market?

Demand is rising because air abrasion systems support minimally invasive tooth preparation, allowing clinicians to remove decayed tissue without the heat, vibration or noise associated with traditional drills. This technique is particularly beneficial for early-stage caries removal, stain elimination, pit-and-fissure cleaning, and composite restoration preparation. The World Health Organization reported in 2022 that untreated dental caries affects billions globally, prompting dental clinics to adopt methods that improve patient comfort, especially for children, anxious individuals and elderly patients.

Air abrasion also supports conservative dentistry. Because the technique preserves healthy tooth structure and reduces microfractures, clinicians prefer using abrasion units for preventive and restorative procedures. Advances in abrasive media, such as aluminium oxide and bioactive powders, have improved efficiency and accuracy. As more dental schools incorporate minimally invasive techniques into training, young practitioners are increasingly adopting air abrasion systems as part of their standard toolkit.

What Are the Obstacles Holding Back Growth in the Dental Air Abrasion Equipment Market?

Despite strong benefits, the market faces several barriers. Initial equipment costs are relatively high compared to those of traditional rotary systems, limiting adoption in small- and medium-sized clinics. Ongoing expenses for abrasive powders and maintenance also increase operational costs. Air abrasion is technique-sensitive, and clinicians require proper training to achieve optimal results, which can be challenging in regions with limited continuing-education programs.

Another restraint is that air abrasion is not suitable for all clinical scenarios. Deep or extensive decay often requires rotary instruments, reducing the applicability of abrasion systems. Dust control and isolation requirements can complicate workflow, particularly in older operatory setups without proper suction infrastructure. Limited patient awareness about minimally invasive alternatives may also slow adoption in developing regions.

What Does the Regional Landscape of the Dental Air Abrasion Equipment Market Look Like?

North America leads the market due to high acceptance of minimally invasive dentistry, strong patient preference for drill-free treatments and widespread availability of advanced dental equipment. Clinics in the United States and Canada increasingly offer air abrasion as an alternative for early caries management and cosmetic microabrasion procedures.

Europe follows closely, supported by strict regulations promoting conservative dentistry and the widespread integration of digital workflows that pair well with air-abrasion techniques. Countries such as Germany, the Nordic region and the U.K. show strong adoption due to robust preventive dental systems.

Asia Pacific is the fastest-growing region, driven by rapid clinic modernization, rising dental tourism, and increasing awareness of patient comfort and atraumatic care. Urban clinics in China, India, Japan and South Korea are increasingly investing in intraoral abrasion units to offer premium patient experiences. Latin America shows steady growth, especially in Brazil, Mexico and Chile, where minimally invasive care is gaining popularity. The Middle East and Africa are expanding gradually through private dental-centre investments, though high equipment costs remain a constraint.

How Is Technology Changing the Dental Air Abrasion Equipment Market?

Technology is playing a major role in improving device precision, control and ergonomics. Modern abrasion units now feature adjustable particle flow, enhanced powder delivery systems, integrated suction ports and finer nozzles for targeted application. Improvements in abrasive materials, including bioactive and remineralising powders, enhance both comfort and clinical outcomes.

Digital dentistry is also reshaping workflows. Intraoral scanners and diagnostic software help clinicians identify early lesions more accurately, increasing the use of air abrasion in preventive interventions. Some manufacturers are developing units with improved LED illumination, digital pressure control and programmable settings for different procedures. AI is beginning to influence cavity detection and treatment planning, guiding clinicians toward minimally invasive interventions that align well with air abrasion techniques. Together, these technological advances position air abrasion equipment as a key tool in the transition toward patient-friendly, conservative restorative care.

Dental Air Abrasion Equipment (Intraoral Abrasion Units) Market Statical Scope

By Product form

- Product form (device hardware)

- Desktop / Cart-mounted (full units with onboard compressor or cart)

- Countertop (compact bench units)

- Portable / Handpiece-only & chair-adapter systems (e.g., single-use tip or mini sandblaster adapters)

- Integrated clinic-suites (units bundled into dental delivery systems)

Rohan Patil stands at the forefront of dental market research, leveraging over five years of specialized experience to navigate the intricate landscape of the global dental industry. As Principal Research Analyst at Towards Dental, he spearheads comprehensive research initiatives that encompass a broad spectrum of dental sectors, including orthodontics, periodontics, prosthodontics, and endodontics.

At Towards Dental, Rohan's expertise extends to analyzing emerging trends in dental technologies, regulatory frameworks, and market dynamics. He is instrumental in assessing the adoption of digital dentistry, advancements in dental materials, and the integration of artificial intelligence in diagnostic and treatment modalities.

Rohan's analytical acumen is complemented by his proficiency in translating complex data into actionable insights, enabling him to provide strategic recommendations that inform decision-making across the dental industry. His work not only supports dental professionals and organizations but also contributes to shaping the future trajectory of dental care globally. A trusted advisor and relentless innovator, Rohan continues to push the boundaries of traditional market research, merging scientific rigor with commercial insight to stay ahead in a fast-evolving dental landscape.

- Mobile Dental Unit Market Size to Attain USD 3.76 Billion by 2034 - January 6, 2026

- Dental Cone Beam CT Market Size to Attain USD 1,247.49 Million by 2034 - January 5, 2026

- Dental Resins Market Size to Lead USD 2.7 Billion by 2034 - January 2, 2026